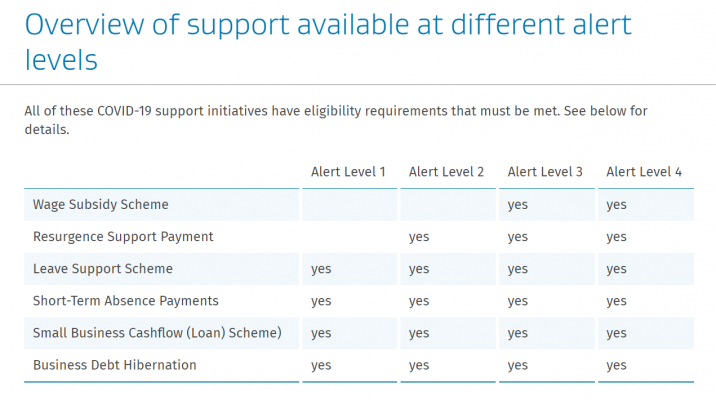

There are various COVID-19 financial support schemes available to businesses, depending on your situation. Learn more about each type of support and where you can find more information.

Resurgence Support Payment

The Resurgence Support Payment (RSP) is a payment to help support viable and ongoing businesses or organisations due to a COVID-19 alert level increase to Level 2 or higher. If your business or organisation is facing a reduction in revenue due to an alert level increase, you may be eligible for the RSP.

Resurgence Support Payment applications will open nationally from 8am on Tuesday 24 August 2021. Applications will remain open for one month after a nationwide return to Alert Level 1.

Businesses and organisations will be eligible if they experience a 30% drop in revenue over a seven day period after an alert level increase and meet other eligibility criteria. This drop is compared to a typical seven-day period in the six weeks before the increase in alert level. Seasonal businesses should show a 30% revenue drop compared with a similar week the previous year.

The decline in revenue must be a result of the specific alert level change, not just COVID-19 in general. You must have been in business for at least six months to be eligible. Charities, not-for-profit organisations, the self-employed and pre-revenue businesses, such as start-ups may also be eligible.

This payment is not a loan, so does not need to be repaid. The payment must be used to help cover business expenses such as wages and fixed costs.

There have been some recent changes to the eligibility criteria for commonly owned groups. A commonly owned group generally consists of businesses that have the same owners. Some individual businesses or organisations within a commonly owned group may now be eligible for RSP. You can find examples of commonly owned groups and more eligibility criteria for the RSP on the Inland Revenue website.

You can also calculate how much you may be entitled to and how to apply on Inland Revenue’s website.

Eligibility for the Resurgence Support Payment(external link) – Inland Revenue

Apply for the Resurgence Support Payment(external link) – Inland Revenue

If you don’t meet the criteria for RSP but do have cash flow problems, Inland Revenue can help. Visit their Manage my tax page for more information.

Manage my tax(external link) – Inland Revenue

Wage Subsidy Scheme

Applications for the Wage Subsidy Scheme are open. You can apply on the Work and Income website.

The Wage Subsidy is a payment to support employers so they can continue to pay employees and protect jobs for businesses affected by the move to Alert Level 4 on 17 August 2021.

The Wage Subsidy is available to eligible businesses, organisations and the self-employed impacted by the move to Alert Level 4 on 17 August 2021.

To reflect higher wage costs since the scheme was first used in March 2020 the payments have been increased to:

- $600 per week per full-time employee

- $359 per week per part-time employee.

Information on the Wage Subsidy Scheme(external link) — Work and Income

Sign up for Wage Subsidy Scheme updates(external link) — Work and Income

Short-Term Absence Payment

A COVID-19 Short-Term Absence Payment is available at all Alert Levels to employers to pay workers who follow public health guidance and are staying home while waiting for a COVID-19 test result. It’s also available to eligible self-employed workers. To be eligible, workers need to be unable to work from home and need to miss work while waiting for the test results.

There’s a one-off payment of $350 for each eligible worker. From 24 August 2021, this payment is increasing to $359 for each eligible worker. Employers or the self-employed can apply for any worker once in any 30-day period.

More information and how to apply(external link) – Work and Income

Leave Support Scheme

The COVID-19 Leave Support Scheme provides a payment to businesses to pay their workers who meet certain health criteria, eg they have COVID-19. This is also available if you’re self-employed.

If you, or your staff have been told by a health official to self-isolate and cannot work from home, you can apply for the COVID-19 Leave Support Scheme.

This support will be paid as a lump sum covering two weeks (you can reapply if required) of $585.50 per week for full-time workers and $350 per week for part-time workers. From 24 August 2021, the payment will increase to $600 per week for full-time workers and $359 per week for part-time workers.

Under changes to this scheme in 2020, businesses are no longer be required to show an actual or predicted revenue drop or that their ability to support an employee was negatively impacted by COVID-19, to be eligible to access the payment.

Leave Support Scheme(external link) — Work and Income

How to apply for the Leave Support Scheme(external link) — Work and Income

Small Business Cash Flow Loan Scheme (SBCS)

Government will provide loans to small businesses, including sole traders and the self-employed, impacted by COVID-19 to support their cash flow needs.

If you’ve previously applied for a SBCS and have fully repaid it, you can apply again.

Applications are open until 31 December 2023. You can apply through myIR.

The small business cash flow loan scheme will provide assistance of up to a maximum of $100,000 to businesses employing 50 or fewer full-time employees. This includes sole traders and self-employed businesses.

Details of the loans include:

- $10,000 to be provided to eligible businesses

- an additional $1800 per equivalent full-time employee

- interest free if the loan is paid back within two years

- an interest rate of 3% for a maximum term of five years

- repayments not required for the first two years

- you must show at least a 30% drop in revenue due to Covid-19, measured over a 14-day period in the past six months compared with the same 14-day period a year ago. If your revenue from the same period a year ago was also affected by COVID-19, compare the same 14-day period two years ago.

- maximum amount you can borrow depends on the number of full-time and part-time employees.

Use the small business cash flow loan scheme eligibility tool and find out how to apply.

COVID-19: Small business cash flow loan scheme eligibility tool

myIR(external link) — Inland Revenue

If your businesses doesn’t have a myIR account, you will need to create one to apply.

Register a myIR account for a business or organisation(external link) — Inland Revenue

Most applicants will receive their loan payment in full from Inland Revenue within five working days. You don’t have to accept the full loan amount you’re offered, and can decide to take a smaller loan.

Tax and ACC support

If you’re having difficulties meeting your tax obligations due to COVID-19, Inland Revenue has various support schemes and options to help.

COVID-19 business and organisations(external link) — Inland Revenue

ACC levy invoices for the 20/21 financial year would usually have been sent from 1 July, but will now be sent in October. ACC has more information about delayed invoices and guidance to help.

Easing the COVID-19 burden on businesses(external link) — ACC

If you are having trouble making ACC payments, ACC has guidance to help. If you are no longer in business, it’s also a good idea to let ACC know.

General COVID-19 information for businesses(external link) — ACC

Business debt hibernation

Business debt hibernation is a government initiative created in response to COVID-19. It helps companies, trusts, and other business entities affected by COVID-19 to manage their debts. Applications are open until 31 October 2021.

If business debt hibernation is right for your business, this is how it helps you manage your debts:

- You set up an arrangement for your existing debts, eg paying your creditors only a percentage of what you owe them on time and delaying the rest.

- You get up to a month of protection while you set up the arrangement, meaning most creditors can’t enforce their debts, eg applying for your business to be liquidated.

- If your creditors agree, you get a further six months of protection.

Use the business debt hibernation decision tool to find out if it’s a good option for your business and if so, how to get started.

The original article is from”https://www.business.govt.nz/covid-19/financial-support-for-businesses/”